In the 1920s the world’s major economies began to move back on to the gold standard, having abandoned it during WW1, because any currency on the gold standard was, according to the ruling orthodoxy of the time, considered ‘stronger’ because its value in gold was guaranteed. This meant that while the UK was on the gold standard anybody who held sterling could at any time demand that the Bank of England exchange their sterling bank notes for the requisite amount of gold. This meant that the central banks were forced to change the quantity of money in the economy depending on the level of their gold reserves, because they always needed to have enough gold to be able to back the amount of their currency that was in circulation.

The operation of the gold standard had many effects one of which was that exchange rates between different currencies were very rigid for long periods. This meant that it was impossible to adjust unbalanced trade via devaluations. Instead what happened was that unbalanced trade (or large capital flows between different currencies) would inevitably mean that gold reserves would rise or fall. Deficit countries would suffer falling gold reserves and surplus countries would accumulate gold. And this meant that central banks were forced to increase and decrease the money supply as gold reserves rose and fell, and in turn this would inflate or deflate the economy.

In fact because it is complex and difficult to actually move large amounts of gold around the real world, the actual gold that the entire monetary system of the world was built upon was only held in a few very secure bank vaults of a few central banks. The real gold hardly moved around at all, all that happened was the notion of who owned the gold changed. Down in the vaults under these central banks there were piles of gold and each pile was labelled with the name of the central bank that owned it. So when, for example, the UK ran a payments deficit with the US it would mean that gold would flow from the UK to the US but in reality all that happened was that in the vaults of the Bank of England a label denoting the ownership of a pile of gold would change. And because this label had changed, because it now read USA instead of UK, the entire UK money supply had to contract and the real UK economy had to endure a process of forced deflation and austerity, and millions of people lost their jobs and countless lives were wrecked. Because the label on a pile of gold had changed.

The terrible absurdities of the gold standard look in retrospect ridiculous. People believed that the entire financial system would collapse if the gold standard was abandoned, in fact the UK abandoned the gold standard in 1931 and all that happened was that the country began to recover from the crash of 1929.

But there are aspects of the current obsession with UK government debt levels that are just as absurd as anything that happened around the gold standard in the 1920s. Consider the question of Quantitative Easing (QE) and its relationship to UK government debt.

Quantitative Easing in the UK

The mechanics of Quantitative Easing (QE) are fairly simple. Central banks can create as much new money as they want by just typing a figure into their electronic ledgers. In order to undertake QE the Bank of England has over a period of time created a lot of new money by just typing it into their computer system and then using this newly created money to buy in the markets various types of bonds and financial assets. Mostly the Bank of England (BoE) has bought UK government bonds.

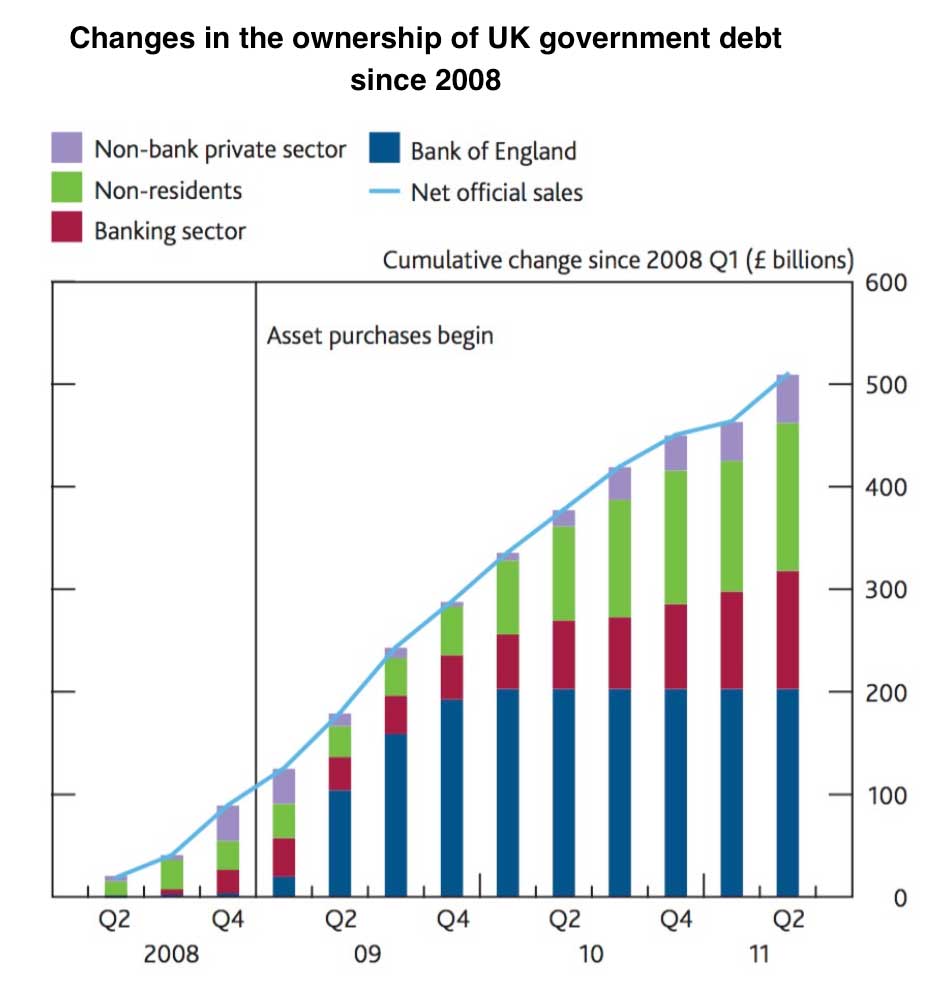

Since the inception of the QE program in 2009 the Bank of England has bought a lot of UK government debt. Between March and November 2009, the BoE purchased £200 billion of financial assets, mostly UK Government debt or ‘gilts’. Since then the BoE has made further purchases: £75 billion in October 2011; £50 billion in February 2012 and £50 billion in July 2012. That brought total assets purchases to £375 billion. There have been no further asset purchases since then. But any funds associated with purchased bonds maturing have been reinvested, so the total stock of QE remains £375 billion.

In order to get a handle on the size and weight of the government debt that the BoE has bought consider that the total purchase of £375 billion of gilts is about equal to 50% of the entire annual spend of the UK government, or that it represents more than the the entire combined annual budgets of the NHS, Education and Welfare.

Even more interesting is to look at that £375 billion of debt purchases in relation to total oustanding current UK government debt which stands at £1,700 billion (as of April 2016). The BoE QE program has bought around 22% of that debt.

This is where things get a bit absurd

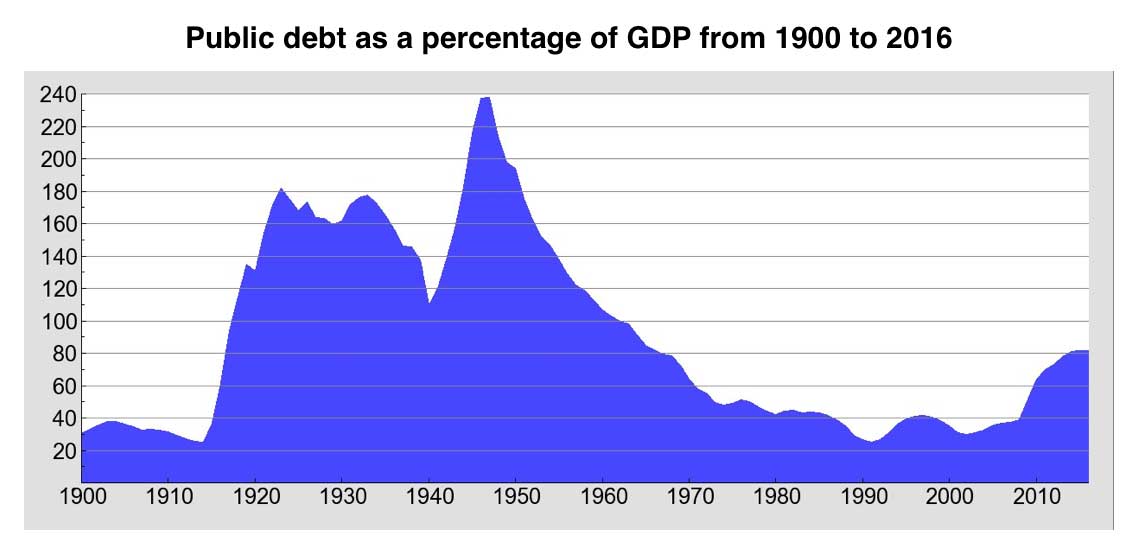

The government constantly goes on and on about the need to reduce government debt. In order to do that it wants to commit, at great cost, to generating an obligatory government budget surplus except in times of recession, so it can ‘pay off’ the debt. I explained in a previous article why running a budget surplus is a bad idea, and by even relatively recent historical standards UK government debt is not that high. As the chart below shows UK government debt was higher than it is now for most of the 20th century, and for long periods it was much higher.

That’s not to say that the 2008 financial crisis did not create a problem for public finances. Bailing out the banks cost a lot, although a lot of that was repaid, and a lot of the huge sums being thrown around were freshly created new BoE money, so although the bail outs caused a one off spike to debt levels the bank bail outs on their own didn’t cause a prolonged problem for public finances. The real problem for public finance was the result of a mismatch between medium and longer spending commitments and tax revenues. The crisis caused a deep recession that caused tax revenues to fall sharply (and welfare paymenst to increase) and it is the fall in tax revenues, caused by low growth, that lies at the heart of the problem of public finances. The huge debt levels of the 20th century were not resolved by generating budget surpluses, they were resolved by economic growth. When the economy grows historically accumulated debt shrinks proportionately.

Consider the commitment to generate a budget surplus to pay off debt in the context of the QE program. In order to generate a budget surplus and to use that surplus to reduce government debt will require drastic and continuing austerity, it will mean shrinking services and lost jobs, and it will deflate the economy (in a similar way that committing to the gold standard led to forced deflation). One percent of the £1,700 billion of government debt is £17 billion. In order to pay off 1% of that debt there would have to be a budget surplus of 2.2%, that is a pretty sizeable surplus, and in order to reduce the total debt by 22% there would have to be a budget surplus of 2.2% every year for 22 years.

And yet through the QE program the BoE has already bought 22% of that debt, which means that the total debt of the UK government has already effectively been reduced by 22%. When the BoE buys government gilts its like they disappear, they cease to have any further economic significance, they become just accounting entries in the BoE books. The interest the government has to pay on those bonds is paid to the BoE who immediately pays it back to the government. There is no requirement for the BoE to ever sell those bonds back to anybody. The only circumstances in which it might be benficial to sell those gilts owned by the BoE is if inflation became a big problem and the economy was overheating in which case the BoE could sell the gilts it holds to suck money out of the economy. But the problem now is not one of inflation and over heating, it is problems of deflation, stagnation and low growth.

The modern post Bretton Woods system of currencies was created in 1971 when the last vestiges of the gold standard were killed off by the Americans when they severed the link between the dollar and gold, and as a result we now live in a global system of fiat currencies. The term ‘fiat currency’ is economist jargon for money that has value just because it is declared by a government to be legal tender, in other words state-issued money which is neither convertible by law to any other thing, nor fixed in value in terms of any objective standard. Modern money is intrinsically valueless and is accepted as money because the government decrees it so, and because people believe in it. The theoretical danger that programs like QE present, programmes which are just printing lots of new money, is that creating too much money out of thin air could lead to inflation, a process that would accelerate if the financial system and the international exchanges markets lost confidence in the currency. But that hasn’t happened.

If the QE was going to create inflation it would have happened when the program was implemented and all that extra money was pumped into the system. It didn’t happen. Now all that is left is an accounting entry inside the BoE. In one column in the BoE ledgers is the total amount of government debt, and it is claimed that this is too high and must be reduced even though this will cause all sorts of real world pain and human suffering. And in another column in the ledger is the entry showing the £375 billion of government debt owned by the BoE.

This where it starts to seem like an echo of moving the labels on the piles of gold back in the 1930s. The government claims that in order to delete £375 billion on both sides of the ledger the government has to carry out a protracted program of austerity. In other words in order to change a ledger entry the entire national economy and public finances has to be changed. The real world has to change – for the worse – in order to match the ledger entry.

Alternatively we could just hit the delete key in both columns of the ledger.

So what would happen if we hit that delete key? What would the reaction be around the world of everyone who holds the other 78% of the government debt? Would not the value of gilts fall through the floor and the interest rates shoot up – meaning that our remaining 78% debt would probably be more of a burden that the previous 100% amount.

I don’t think anybody knows what would happen if the delete key was clicked. The economic impact of (effectively) printing lots of money to buy those gilts (and its the printing of the money that it is claimed leads to inflation and currency damage) has already happened and the result is that the yields on gilts continue to fall and inflation is very low.

In reality publicly hitting the delete key would probably produce some sort of reaction in the markets. More sensible would be the public acknowledgment that the 22% of debt held by the Bank of England has a special status and should be accounted for separately from the rest of UK debt. Perhaps announce that it will be held for a long, long time, possibly for decades and that therefore it should be accounted for separately from the rest of the debt that is owned by other entities.

Either way the least sensible thing to do would be to either sell the debt (unless inflation was shooting through the roof and the money supply had to be shrunk very quickly – which seems under current conditions to be unlikely) or the BoE owned debt is counted as part of the rest of the debt and real austerity and deflation was imposed in a ridiculous effort to generate a surplus and pay off the debt.

Comments on this entry are closed.