China has been running a very large trade surplus for over a decade. The Chinese surplus is part of the significant imbalances in the Chinese economy, imbalances which cannot be sustained and which are already in the process of being painfully adjusted (see this article for a detailed analysis of these imbalances). The Chinese government held down the exchange rate of the renminbi for many years in order to keep its exports cheap and to foster the growth of a large trade surplus. The way the People’s Bank of China (PBC), which is China’s central bank, held down the value of the renminbi was by selling it and buying foreign exchange, including over a $1 trillion worth of U.S. Treasury bonds. This meant the PBC built up over $3 trillion of foreign-currency reserves.

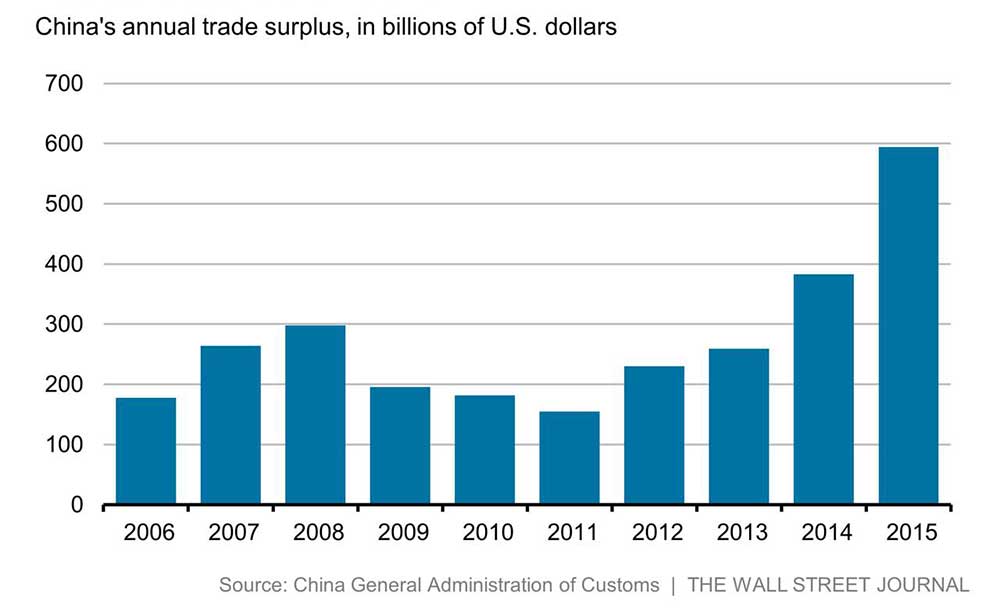

The Chinese trade surplus swelled by 55% in 2015, to $595 billion. In terms of Chinese economic performance this isn’t actually as good as looks, it doesn’t reflect a boom in exports, which for the full year actually fell by 2.8%, the surplus widened because imports fell even more, by 14.1% (signs of a slowing Chinese economy).

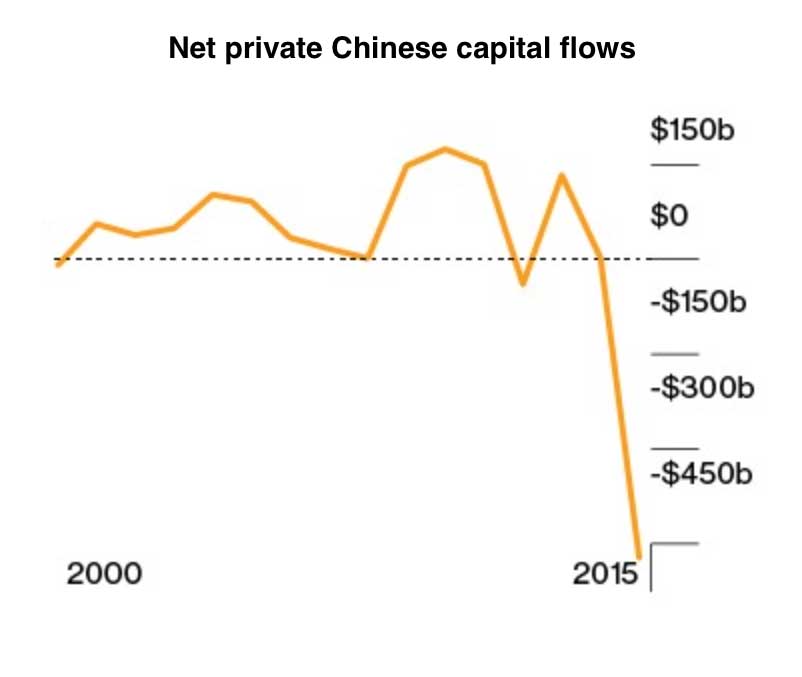

Given this growing and huge trade surplus how did China manage to post a decline of $513 billion in foreign-exchange reserves last year? Since a trade surplus brings foreign currency into the country, and most exporters turn that currency over to the central bank, it should boost reserves by a corresponding amount. The reserves fell because non-trade related fund outflows were large enough to overwhelm even that trade surplus.

A combination of factors, including slowing economic growth and a gradual relaxation of restrictions on investing abroad, has unleashed a torrent of capital outflows.The world’s largest currency hoard decreased by $99.5 billion in January to $3.23 trillion, according to a People’s Bank of China statement released on Sunday. The stockpile slumped by more than half a trillion dollars in 2015, the first-ever annual decline. Capital outflows increased to $158.7 billion in December, the most since September and were $1 trillion last year, according to estimates from Bloomberg Intelligence. That’s more than seven times the amount of cash that left in 2014.

Private citizens are now allowed to take up to $50,000 per year out of the country. If just one of every 20 Chinese citizens exercised this option, China’s foreign-exchange reserves would be wiped out. Beijing is at the same time trying to boost domestic liquidity in the hopes that this will generate stronger domestic demand, but expanding liquidity fuels capital outflows as people and businesses take the opportunity to move funds abroad. At the same time, China’s cash-rich companies have been employing all sorts of devices to get money out. A perfectly legal approach is to lend in renminbi and be repaid in foreign currency. A not-so-legal approach is to issue false or inflated trade invoices – essentially a form of money laundering. For example, a Chinese exporter might report a lower sale price to an American importer than it actually receives, with the difference secretly deposited in dollars into a US bank account.

Now that Chinese firms have bought up so many US and European companies, money laundering can even be done in-house. The Chinese hardly invented this idea. After World War II, when a ruined Europe was smothered in foreign-exchange controls, illegal capital flows out of the continent often averaged 10% of the value of trade or more. As one of the world’s largest trading countries, it is virtually impossible for China to keep a tight lid on capital outflows when the incentives to leave become large enough.

China is struggling to formulate a consistent currency policy and to prevent the large scale capital exports from turning a controlled decline in the value of the Chinese currency into an old-fashioned run on the renminbi. When the central bank overhauled its policy in August, its stated aim was to give market forces a greater role in determining the exchange rate, with a view to securing the renminbi’s inclusion in the International Monetary Fund’s special drawing rights basket, alongside traditional reserve currencies. But it swiftly found itself forced to prop up the currency, spending a sixth of its foreign exchange reserves in five months. This reflects the scale of capital flight under way as lower interest rates, worries about the economic outlook and the clampdown on corruption drive Chinese people to take their wealth out of the country. The IIF, the chief global body for the financial industry, calculates that capital outflows from China reached $676bn last year. The central bank has been burning through foreign exchange reserves to offset the bleeding and shore up the currency, culminating in intervention of $140bn in December, by some estimates.

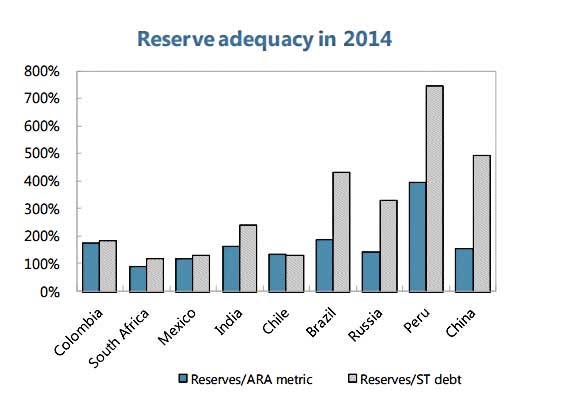

China’s $3.3 trillion foreign reserves actually fall to the bottom end of the safe band under the International Monetary Fund’s measure of reserve adequacy (a metric known as known as ‘Assessing Reserve Adequacy’ or ARA) and are relatively low by emerging market standards, given that Beijing is trying to defend a semi-fixed exchange rate and do so within a framework of heavy capital flows. The Philippines, Thailand, Peru, Brazil, India and even Russia score higher. The IMF recommends a band of 100pc to 150pc under its complex ARA measure. China is currently near 120pc and almost certainly fell further in January. Using the IMF guidelines as a measures shows that China needs reserves of at least $2.75 trillion in order to ensure financial stability. If the reserves fall below $2.75 trillion Beijing will lose operational flexibility. The country has roughly $600bn left – at the most – before it finds itself in a very uncomfortable situation.

The IMF has developed a suggested framework based upon research into previous currency crises. According to this formula, countries should maintain reserves equivalent to the sum of 30 percent of their short-term foreign-denominated debt, 15 percent of other portfolio liabilities, 10 percent of the M2 or broad money supply and 10 percent of yearly exports. In China’s case, that would add up to approximately $3 trillion. The biggest share comes from M2, which in China totals approximately $21 trillion. Currently, even China’s seemingly huge reserves amount only to 15 percent of M2 money supply, the lowest proportion since 2008; even if that share were lowered to 10 percent, China would still need $2.1 trillion to cover it. Covering short-term foreign debt, portfolio liabilities and yearly exports would add another $900 billion.

At current rates, China will drop beneath the recommended amount of $3 trillion at the end of the first quarter even if including all illiquid assets; excluding them, China could have fewer than $2 trillion in usable reserves by summer. By the end of the year, the government could face a situation where the only tools left to prevent the currency’s slide could be hard capital controls that prevent money from leaving the country — an embarrassing state of affairs for the world’s second-largest economy.

The Chinese central bank is automatically tightening monetary policy as it runs down reserves, adding to the growing pressure on Chinese banks already fragile because of the large and growing volume of bad debts on their books. This is not something that can continue for very long. The more the PBC expends its reserves to resist downward pressure on the currency, the more they will shrink the money supply, a dangerous thing to do given the scale of bad debt inside the Chinese banking system.

Despite the giant trade surplus the People’s Bank of China has been forced to intervene heavily to prop up the exchange rate – so much so that foreign-currency reserves actually fell by $500 billion in 2015. With such leaky capital controls, China’s war chest of $3 trillion won’t be enough to hold down the fort indefinitely.

There is a lot of market speculation that the Chinese will undertake a sizeable one-time devaluation, say 10%, to weaken the renminbi enough to ease downward pressure on the exchange rate. But, aside from providing fodder for the likes of Donald Trump, who believes that China is an unfair trader, this would be a very dangerous choice of strategy for a government that financial markets do not really trust. The main risk is that a big devaluation would be interpreted as indicating that China’s economic slowdown is far more severe than people think, in which case money would continue to flee. If the PBC ever were to stop intervening, and to let the renminbi depreciate to some imagined fundamental “equilibrium”, it would quickly see that there is no such equilibrium level. In a speculative market, the market does not tend towards some stable value, with self- dissipating movement in any one direction reducing pressure for further movement in that direction. Price movements instead are self-reinforcing, and can quickly overshoot fundamentals.

Currency uncertainties like those that surround the renminbi have inevitably attracted the attentions of currency speculators whose interventions in the market can by themselves help create the conditions for a forced renminbi devaluation from which the speculators hope to profit.

China took strong action in January aimed at curtailing the activities of offshore speculators betting against its currency. But it is merely attacking a symptom, not the root causes, of its currency woes.

China’s central bank intervened aggressively in the market for renminbi traded offshore—mostly in Hong Kong which is known by traders as ‘CNH’. Asserting control over the CNH market was simple. Total CNH deposits in Hong Kong in November stood at 864 billion renminbi ($131 billion at current exchange rates). That is easily overwhelmed by China’s $3.33 trillion of foreign-currency reserves. Acting through state-owned banks, in January the People Bank of China bought massive quantities of CNH, successfully closing the yawning gap that had opened up between the renminbi’s value in Hong Kong and in mainland China.

This gap—during early January the CNH was trading at a discount of more than 2%—was a source of embarrassment to the People’s Bank of China. It showed that international markets were spooked, and didn’t believe its assurances that there is “no basis” for continued renminbi depreciation.

Beijing essentially squeezed the market into dysfunction. Within in days of the PBD intervening the cost of borrowing CNH overnight in Hong Kong soared to almost 70%, making it prohibitively expensive to keep betting against the currency. Given that China can step in anytime to disrupt renminbi trading, shorting the renminbi could be hazardous in the near term. But given the scale of Chinese capital exports the long-term direction for the currency is still to the downside.

This action comes at the cost of a long-term policy objective: to foster a vibrant offshore market for the renminbi, eventually making it a widely used currency world-wide. By engineering a liquidity squeeze, China has introduced new risks into the offshore market that will make it less attractive to investors. As always, maintaining control is Beijing’s priority, and other goals come second.

Chinese officials managing the situation have few attractive options. They could carry on using official reserves to prop up the renminbi, which would have fallen more steeply without central bank intervention. But even China, with its $3.3tn stockpile, cannot burn reserves at that rate indefinitely. They could adopt tighter capital controls, reversing the thrust of recent liberalisation. They could let the renminbi go but risk a steep depreciation that would be a shock to the global economy. Few would contemplate the economic cost of raising interest rates to support the currency.-

The problem of managing its currency is part of a larger and far more difficult strategic dilemma facing the Chinese leadership. The problems of managing the exchange rate is similar to the problems that the leadership have faced when the Chinese stock markets began to collapse last year. In order to restructure the economy and prevent the deep economic imbalances from triggering a debt crisis and a disorderly harsh adjustment which could trigger political instability the Chinese government must give up controlling key mechanisms in the economy (such as the exchange rate) which means losing control of events and therefore risks political instability. They are between a rock and a hard place.

And underneath all the specific headline grabbing mini-crises such as the stock market crashes and the currency problems lies the big and deep problem which is that the Chinese growth model is no longer sustainable. China’s most serious problem is “the relentless accumulation of debt”, and economic conditions will continue to deteriorate until Beijing directly addresses the debt. In fact it doesn’t really matter if China is able to report growth rates for another year or two of 7%, or 6%, or even 8%. If the only way it can do so is by allowing debt to grow two or three times as fast (which is what has happened in the past and will happen in the future), there will have been no improvement at all, the economy will not have adjusted, and China’s longer-term outlook will be worse than ever.