The issue of the UK economy and how best to recover from the damage done by the Great Recession is the central issue of national politics. The narrative promoted rigorously by the Tory government and the Chancellor George Osborne is that the country was almost bankrupted by the Labour government and that slowly but surely, under his wise guidance, it is recovering.

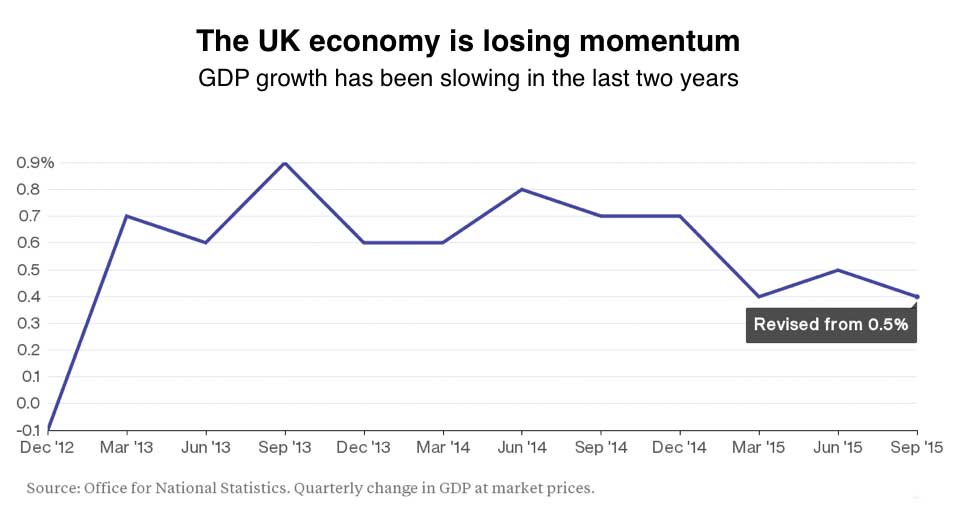

So how well is the UK economy doing and how will it develop over the next few years, have we left the recession behind and are we at last on the road of consistent and strong growth? The Office for National Statistics announced on the 23rd of December that the gross domestic product of the UK rose 0.4 percent between July and September instead of the 0.5 percent previously estimated. Growth in the second quarter was revised down by 0.2 percentage points to 0.5 percent. The revisions indicate a loss of momentum in an economy that continues to rely heavily on consumers and domestic demand. The UK government claims that its economic strategy will deliver continuing growth and a reduction in the government deficit leading to a balanced budget by the end of this parliament in 2020. How plausible is this forecast?

Two recent reports, one from the EREP network and one from Centre for Business Research, have examined critically the claim that the UK is doing well and both have come to more pessimistic conclusions about the health of the UK economy.

The EREP network (Economists for Rational Economic Policies) has published its Review of the UK Economy in 2015 (download the full report here), with a series of short articles focusing on different aspects of the UK economy. The Review argues that:

“Despite the increase in those in some form of employment (as employee or self-employed), the wage pressures are far from strong, and real wages remain far below their peak in 2008. This trend to lower pay has weakened demand and productivity. Whilst commodity and producer deflation have enabled shoppers to buy more goods for the same money, it is notable that people are not spending much more. On the contrary, in recent months, we have seen unsecured private debt mounting, as people once again resort to borrowing to get by.

As the year has progressed, the economy has slowed and regressed. The public finances are built on hopes and assumptions that appear to be fragile indeed, and economic activity in many key areas has decelerated whilst the property boom helps the asset-rich. The weaknesses in the UK economy are more and more apparent, like a building with a flashy design but poor construction. The cracks begin to show. Let’s hope there’s no earthquake coming…”

Modelling the UK economy

The UK Government’s economic strategy is intimately entwined with economic forecasts. The Charter for Budget Responsibility ties the Government into balancing its budget by 2019/20, and the forecasts of the Office for Budget Responsibility (OBR) assess whether the Government is on course to meet this fiscal objective. The political importance of the OBR forecasts is reflected in the fact that the OBR was mentioned ten times in the Chancellor’s 2015 Autumn Statement speech and the Director of the OBR was thanked by name. The Bank of England uses its own DSGE model for forecasting the performance of the UK economy which, although it produces somewhat different outcomes than the OBR projection, is broadly in line with OBR projected UK growth rates.

The accuracy of these projections are of more than academic interest because the entire current Tory government strategy hinges on achieving steady and continuing growth in the UK economy which will, after the ‘necessary’ pain of austerity, deliver a reduction in government debt and borrowing whilst achieving growth and a buoyant job market. The success of the government’s economic strategy is what is expected to underpin the succession of Osborne to the party leadership and another election victory against a weakened Labour Party in 2020.

The OBR forecasts to 2020 claims to include a projection of the consequences of the Tory government’s plan to reduce the fiscal deficit, but the OBR model does not include any feedback from fiscal policy to aggregate GDP in the sense of a Keynesian multiplier. Since there is no such feedback, austerity appears in the OBR model to have no adverse consequences for aggregate output or employment. The relaxed public reaction to the austerity plans, and indeed the Conservative victory in the 2015 general election, are influenced by the OBR’s judgement that fiscal austerity can be combined with favourable economic growth.

The OBR forecasts are driven by neo-classical supply-side assumptions in the form of a modelled trend of growth of productive capacity and an assumed rapid convergence of GDP towards this trend. In other words the OBR model assumes that the economy’s equilibrium state, all other things being equal, is to settle into steady growth. Productive capacity is not measured directly by the OBR but is assessed as current GDP plus an ‘output gap’ the size of which is measured from surveys of businesses. The future growth of productive capacity is modelled by making assumptions about the ‘natural rate’ of growth under various conditions. Assumptions about productivity growth are combined with projections for the expansion of labour supply (where migration projections depends on Office of National Statistics assumptions).

Since the UK economy is currently judged to be close to full capacity, the OBR’s forecasts for GDP are the same as its assumed path for productive capacity, i.e. a growth of close to 2.4% per annum, essentially forever. In the OBR model fiscal austerity makes no difference. Any fall in public spending is automatically compensated for in the private sector (this belief that there is always a trade off between public and private spending is a deep assumption of neo-classical theory), including an unprecedented five-year run of business investment growing at 6% per annum.

So how good are the these economic projections from the OBR and the Bank of England?

An alternative model of the UK economy

The Centre for Business Research (CBR), which is a research institution within the University of Cambridge conducting interdisciplinary research on enterprise, innovation and governance in contemporary market economies, has just published a critical report which argues that both the OBR and Bank of England models are unrealistic and that the UK economy is likely to perform worse than is projected.

The Centre for Business Research (CBR) finds in its report that the OBR’s approach to modelling is unhelpful and unrealistic, and as a result it has a relatively poor forecasting record and, of course, is incapable of projecting a major downturn or crisis except as resulting from some sort of an exogenous shock (see the background note below). The DSGE model of the Bank of England is in the CBR view even more unrealistic, with a worse forecasting record.

The dominant neo-classical economic discourse of the last few decades is founded upon the belief that economic and financial systems are inherently self stabilising and that unless they are hit by external shocks of some kind (a war, political upheaval, intrusive state regulation, disruptive technology change etc) they will settle, if left alone, into a state of equilibrium and steady growth. One powerful counter theory came from the work of the great analyst of financial crises the economist Hyman Minsky, who died in 1996, and whose work was almost forgotten during the hubris of the Great Moderation but who has since the financial crisis of 2007 been rediscovered. His ‘Financial Instability Hypothesis’ proposed that the system itself could generate shocks through its own internal dynamics. He believed that during periods of economic stability, banks, firms and other economic agents become complacent. They assume that the good times will keep on going and begin to take ever greater risks in pursuit of profit. So the seeds of the next crisis are sown in the good time. Minsky argued that long periods of economic stability, by allowing ever more dangerous speculative activity to build up, led inevitably to a ‘Minsky Moment’ (although he himself did not actually use that term) when the speculative bubble bursts and a financial crisis erupts. There is nothing like the Minsky concepts in the OBR model. The largest ‘Minsky Moment’ since the Great Depression occurred in 2008.

As a result of dissatisfaction with the shortcomings of the OBR and Bank of England models, the The Centre for Business Research have spent the last three years constructing an econometric model of the UK economy following a broadly Keynesian framework, and based loosely on the post-Keynesian ideas of contained in Wynne Godley and Marc Lavoie’s ‘Monetary Economics’ theories (see here and here).

Using the theoretical framework developed by Wynne Godley and Marc Lavoie the CBR model includes the impact of borrowing and debt on household consumption and investment, and recognises the importance of what Claudio Borio of the Bank for International Settlements (the global central bank of central banks) calls ‘financial super-cycles’. These are credit cycles, which in the UK have tended to last for around 20 years. The CBR view is that the fourth post-war financial super cycle began in 2012 and it is the upswing of this cycle that is generating the economic growth that offsets the impact of public sector austerity. The CBR projection is that the credit cycle will slow over this parliament and peak around 2020.

What is a “financial super cycle“? While “there is no consensus on the definition,” according to Claudio Borio, it can be understood as a sequence of “self-reinforcing interactions between perceptions of value and risk…which translate into booms followed by busts.” This corresponds with large increases and decreases in the amount of private debt relative to income, as well as the prices of assets financed by that debt, such as property. For Claudio Borio, the financial cycle has several salient features that often cause it to be ignored by mainstream economists. First, it has a much lower frequency than a typical business cycle. Instead of going from peak to trough every 5-7 years, the financial cycle can take decades. Patterns of economic activity on both the upside and downside simply do not make sense unless the high-frequency business cycle is overlaid on top of the slower-moving financial cycle. Second, the amplitude of the financial cycle is very wide compared to the amplitude of the normal business cycle. This combination means that the financial cycle produces sustained booms and deep downturns.

A slowing credit cycle combined with cuts in government spending leads the CBR to forecast that UK GDP growth will slow to a little over 1.0% per annum by the end of this decade and remain slow there-after. This is much lower growth than the OBR and the UK government is projecting. Slow growth in GDP, combined with higher interest rates and the recent upturn in wage growth will, in the CBR’s view, lead to an end to the jobs boom which has been such a remarkable feature of the UK economy since 2012. Since the CBR does not assume that the UK will leave the EU, their expectation is that immigration will continue at a high level even without much growth in jobs, just as it did in 2009. The combination of low job growth and high immigration means that the CBR expect unemployment to begin rising once more after 2017.

One of the most dramatic aspects of the CBR forecast is an end to the job creation boom of 2010-16. The CBR expects 2.5 million additional jobs will have been created in this boom by 2016, but forecasts employment growth to slow in 2017 and to fall in 2018 and 2019. The long fall in the unemployment rate from its 2011 peak is also projected to end in 2016 at a low of 4%, and to begin rising in 2017 to new peak of close to 7% by 2020. Again these forecasts are very different from those published by the OBR which projects 600,000 more jobs by 2020 than in the CBR baseline projection, and an unemployment rate settling at a little over 5% in all future years. The difference between the CBR unemployment forecasts and those of the OBR is only partly a reflection of contrasting views about the future of jobs. Around half of the unemployment gap is due to different views about future levels of net working-age migration. The CBR forecast for net migration is at over 300,000 in every year up to 2020, compared with a past average of 215,000 between 2010 and 2014. The OBR’s unemployment forecast is consistent with a net migration rate of around half of the CBR’s, at 160,000 a year. With pressures on immigration into the UK remaining strong, the CBR view is that the OBR are unrealistic in assuming that net migration will fall to little over half of the 2014 level.

With falling government spending, in the view of the CBR the only thing preventing near recession in 2018 and 2019 is the high level of household borrowing. The CBR expects the number of housing loans to peak at over 1.2 million by 2018, and to drive house prices higher, reaching an expected peak ratio of mean house prices to post-tax household income of a wholly unprecedented 17 times incomes by 2020. This compares to a ratio of 12 in 2010 and a low of 8 in 1996. Loosening credit conditions are projected to result not only in high levels of mortgage debt but also similarly high levels of short-term unsecured debt. Aggregate household debt would, under these conditions, reach a level of close to two times post-tax income in 2020, a third above today’s level and double the level of 1996. This high ratio is not solely due to a high level of borrowing, but also to a low projected growth of household incomes.

The economics of austerity in government spending means that growth in incomes is repressed by the multiplier effect of cuts in public spending. Growth in GDP can be maintained if expansion in consumption and investment by households is maintained by borrowing. Eventually, levels of household debt and house prices become unsustainable. This is not because debt repayments become particularly high by historical standards. At a projected level of just over 5% of disposable income by 2020, the debt interest payment rate, although double the level in recent years, would be close to the average for the 1990s. The problem arises rather in the housing market where it becomes difficult to sustain extraordinarily high house prices, out of line with all historic experience.

The housing market has been partly sustained by buy-to-let purchasers, partly fuelled by demand from from migrant tenants, but rents cannot continually rise relative to incomes. At some point prices will cease to rise, and expectations of future price increases will fade. In these circumstances a sudden collapse in house prices can easily occur as it did in 2008-9. The possibility of defaulting loans then puts banks under pressure. Something similar happened in 2008-9 at much lower levels of both household debt and house prices than the CBR expect by 2020.

| The CBR projections show GDP growth declining and by 2020 household consumption and wages growth slowing to below inflation (i.e. falling in real terms), and unemployment rising | ||||||

|---|---|---|---|---|---|---|

| Percentage change per annum | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

| GDP | 2.7 | 2.2 | 2.0 | 1.7 | 1.1 | 1.3 |

| Household Consumption | 4.4 | 4.3 | 3.3 | 3.0 | 2.3 | 1.7 |

| General government consumption | 0.1 | 1.0 | 1.8 | -0.3 | -0.3 | 1.5 |

| Business investment | 5.8 | 5.2 | 1.0 | -0.2 | 0.1 | 1.4 |

| Government investment | 3.1 | 0.6 | 0.6 | -1.6 | 1.9 | 2.0 |

| Household investment | 11.2 | 30.6 | 4.9 | -0.2 | -2.6 | -3.3 |

| Exports | 2.7 | 0.8 | 1.9 | 3.9 | 3.4 | 3.7 |

| Imports | 5.4 | 5.7 | 4.1 | 3.2 | 3.2 | 3.6 |

| Inflation | 0.0 | 1.2 | 1.5 | 2.3 | 2.8 | 2.7 |

| Employment | 2.1 | 1.5 | 0.7 | -0.4 | -0.7 | -0.6 |

| Average earnings | 3.6 | 4.6 | 3.5 | 3.6 | 2.3 | 1.2 |

| Unemployment | 4.9 | 4.0 | 4.1 | 50. | 5.9 | 6.8 |

A growth alternative to austerity

The CBR proposes an alternative strategy to what it sees as the unsustainability of growth underpinned by expanding household borrowing, an alternative based on a ‘reflation’ scenario in which government current and capital spending on goods and services grows much more rapidly than in existing government plans. The CBR have selected the largest increases in spending compatible with inflation at under 4% per annum and a ratio of public sector debt to GDP not exceeding its 2016 peak at 81%2. This generates a cumulative £160 billion of additional real government spending on goods and services by 2020 and over £400 billion by 2025. In this scenario real GDP grows 0.5% per annum faster on average up to 2020, and unemployment remains close to 4.5%, and 700,000 lower than in the baseline projection by 2020. The result leaves government debt higher than in the baseline forecast, but gives a more balanced outcome for the household sector. The ratio of house prices to incomes is much lower by 2020 than in the projection bases on current government strategy. Household debt is also somewhat less extreme than in the current government strategy, although it is forecast to be above the previous peak level of 170% of average disposable income.

The CBR concludes that neither the forecasts based on current government strategy nor the reflation scenario do much to regain lost output since 2008. In both cases GDP per head in 2020 is close to 20% below the pre-2008 trend, with the gap continuing to rise thereafter. This demonstrates the limits of action in a single country within a globalised economy with a substantial international deficiency of demand. Reflation in the UK alone would leave price inflation at just under 4% per annum and public sector debt at close to 80% of GDP. Unemployment would be projected to be much lower, for at least a decade, but per capita incomes would be only a little higher.

Whether the outcomes under the reflation scenario with faster growth and lower unemployment are preferred to an austerity approach, which results in lower inflation and lower public sector debt, will be a matter of political preference. Both approaches carry dangers, but they are of different types. While public sector austerity runs a real risk of another private sector financial collapse and recession, a reflationary approach carries the difficulties of managing a high public sector debt if a major economic shock were to spread to the UK from abroad. The CBR emphasises that the reflationary strategy produces neither a continually rising public debt ratio nor increasing inflation, which economists assessing fiscal reflation have often most concern. The present Government and its supporters emphasise the dangers from high government debt but largely ignore the dangers from high household debt.

A much superior approach for satisfactory economic growth in a balanced manner would involve co-ordinated demand expansion across all of the major economies but with the waning of US hegemony there does not appear to be a global centre of leadership capable of delivering such a complex project. During the recent financial crisis China supported global demand, but as it restructures its economy (see here and here) Chinese growth is falling rapidly and is already depressing commoidty markets and many commodity dependent emerging economies. The policy choice of governments in the USA, UK, and especially the Eurozone, to opt for austerity makes it difficult for any single economy to reflate alone.

Much of course depends on the wider economic environment. The CBR forecasts are conditional upon assumptions about the growth of world trade and US interest rates. The CBR do not forecast international economic conditions themselves, instead the CBR uses forecasts for UK-weighted world trade from the Oxford Economics world model. The Oxford Economics model project an improving growth rate for world trade, rising to 5% per annum in 2017 and 2018 but growing in the longer term at 4% per annum, a rate which is well below the historic average of over 6% per annum. The outcome is almost certain to be more volatile than this forecast, and dependent on unforeseeable political and economic global circumstances, not least the uncertain outcome of the ending of the Chinese investment driven growth model and a resulting wrenching economic restructuring. Such volatility would affect the UK’s economic future but not necessarily change the average growth path. For US interest rates the CBR rely on itsour own assumption that short-term rates will slowly rise to 3% by 2019 and remain at that level. Once again, if the actual path is different the UK forecasts would change.

The long term significance of the crash of 2008 and the Great Recession that followed it

The CBR forecasts that per capita GDP continues to diverge from the pre-crisis trend which had been followed for at least 60 years. The dislocation in this trend is the most important macroeconomic phenomenon of our times. For reasons not fully clear, the UK economy is now on a much lower growth trajectory than for the whole of the previous period since WW2. One important consequence is the ‘need for austerity’. GDP in 2015 is 16% below the pre-2008 trend, and hence government tax revenues are reduced by a similar amount or around £125 billion per annum. The apparent need for large cuts in public spending, in an attempt to return to the relatively small deficits of the pre-crisis years, stems from a failure of the economy to return to the long-term growth trend as happened in all previous recessions. Osborne plans to reduce the deficit further, to zero by 2019/20, but in the view of the CBR he will not achieve this aim.

The dislocation to long term growth trends caused by the 2008 event, and the affects this had on eroding the revenue base of the public sector, meant that the economic and fiscal policies pursued under New Labour would have had to change, but so far it is the Tories that have reaped the political advantage from the 2008 crisis and have set the agenda for the reshaping of the post 2008 economic landscape based on shrinking the state, reducing the deficit and balancing the budget. After the defeat of 2010 the Labour Party, in a moment of extreme political madness, accepted and therefore legitimised the Tory narrative that the main problem was overspending under New Labour, and the continuing crippling effect of this profound political misstep has meant that so far Labour has utterly failed to come up with a viable alternative narrative. However if the CBR projections are accurate then the Tories economy narrative is going to run into trouble as it fails to deliver either sustained growth, improved living standards or a balanced budget.

The slow growth projected in the CBR forecasts would reduce the flow of tax revenues and lead the Government to miss its target for a zero deficit by 2019/20 with public sector debt remaining well above the OBR’s expectation that it will fall to 71% of GDP by 2020. One of Wynne Godley’s beliefs was that governments cannot control their deficits or debt, since their revenues depend on growth in private sector income. In the current circumstances the Chancellor is, in the view of the CBR, relying on the expansion of household debt to generate the revenues necessary to cut government debt. The CBR forecasts show that although the Osborne’s austerity program may help to reduce the public finances deficit in the short term it is built on a consumer credit boom and escalating house prices that will lead to yet another boom bust cycle.

In other words – current UK growth is being driven by rising private debt which is balancing the deflationary impact of cuts in UK government spending and debt. Once the private debt cycle reaches the point of exhaustion (which in the CBR view is relatively soon) growth will slow and, combined with the deflationary impact of government spending cuts, this will cause growth to slow which in turn will cause the erosion of the government’s fiscal position, and this in turn will cause the government to miss its deficit reduction targets. This could seriously undermine the popularity of an Osborne succession and render the Tory government vulnerable to attack, assuming of course that the Labour recovers its wits and begins to function as an effective opposition and a viable government in waiting. Unfortunately I don’t think the Labour Party will recover its wits anytime soon and as a result I fear that the opportunity to attack the Tory government a few years down the line, at a moment of vulnerability as it’s economic policy runs into the buffers, will probably be lost.

If in a few years the Tories’s economic strategy runs into difficulties, and if, as I fear, Labour proves incapable of offering both a strong critique of that policy and a powerful, plausible and viable alternative economic narrative, it would represent a generational failure by the left.