The Eurozone is over fifteen years old. How is it doing?

The currency was introduced in non-physical form (traveller’s cheques, electronic transfers, banking, etc.) at midnight on 1 January 1999, when the national currencies of participating countries (the eurozone) ceased to exist independently. Their exchange rates were locked at fixed rates against each other. The euro thus became the successor to the European Currency Unit (ECU). The notes and coins for the old currencies, however, continued to be used as legal tender until new euro notes and coins were introduced on 1 January 2002.

The Eurozone Crisis broke out in May 2010; it is a long way from finished. Although some sort of stability has returned to the eurozone recently, growth and unemployment in the eurozone have never recovered from the crisis and remain at very depressed levels, and are expected to remain depressed for years to come. The creation of the single currency was intended to act as a major driver of political union but in fact the tensions and economic problems caused by the euro have actually undermined European solidarity and is a major factor in the fragmentation of European politics and the rise of nationalist and radical political forces in the EU. The economic malaise is feeding extremist views and nationalistic tendencies just when Europe needs to pull together to deal with challenges ranging from the migration crisis, tensions with Russia in the east and possible new financial shocks.

Meanwhile a large slice of Europe’s young people have been or will be jobless during the critical, formative years of their working lives and unemployment rates, which are high across the zone, are at depression era levels in several eurozone member states.

Worse yet, many of the fragilities and imbalances that primed the monetary union for this crisis are still present. The European banking system remains weak and investment levels remain very low. Many of Europe’s banks have still not recovered from the financial crisis and face problems of non-performing loans. Many banks are still heavily invested in their own nation’s public debt, a tie that means problems with banks threaten the solvency of the government and vice versa (see my description of how the the Euro and the European banking system combined in to a ‘doomsday machine’ that exploded in 2010).

Even though interest rates are essentially at zero across the eurozone, and some government bonds actually have negative interest rates, and even though the ECB belatedly embarked on a large scale Quantitive Easing program, economic activity and credit creation remains depressed. That means borrowers across the Continent are vulnerable when the near-zero interest rates start to rise and the cost of their debt starts to rise and in the meantime the years of near-zero interest rates have undermined the financial viability of corporate investors such as pension funds.

The causes of the eurozone crisis

Behind virtually every economic crisis is the rapid unwinding of economic imbalances. This was the case with the eurozone crisis, the imbalances that caused the crisis were were not particularly original, it was too much public and private debt borrowed from abroad and uncorrected trade imbalances.

From the euro’s launch until the financial crisis in 2008 two complimentary and deep imbalances developed in the eurozone. On the one hand very large imbalances in trade developed with some countries (Germany, Netherlands, etc) running very large current account surpluses, and other eurozone countries (the southern periphery) running very large deficits. These trade imbalances were ‘balanced’ by very big capital flows from countries like Germany, France, and the Netherland to eurozone periphery nations like Ireland, Portugal, Spain and Greece.

The capital flowing into the deficit countries was not invested productively, such capital flows rarely are, but instead fuelled speculative property bubbles, and in the case of Greece burgeoning public debt. This meant that productive assets were not being created to pay off the borrowing, and thus rebalance the balance of payments, instead the speculative bubbles and Greek government debt tended to drive up wages and costs in a way that harmed the competitiveness of the receivers’ exports and encouraged further worsening of their current accounts. It was a vicious circle but while the imbalances were growing the peripheral countries of the eurozone seemed to be growing very strongly, it seemed as if the banks in countries like Germany and France had made sensible secure investments in the south, and that the whole single currency project had been a great success.

The eurozone crisis was a ‘sudden stop’ crisis

The eurozone crisis was, like most economic crisis, caused by prolonged economic imbalances building up over time, and again like most crisis, the actual crisis was triggered by a sudden stop in the financial flows that had sustained the imbalances.

It is important to note that the eurozone crisis was not a government debt crisis in its origin even though it evolved into one. Apart from Greece, the nations that ended up with bailouts were not those with the highest debt-to-GDP ratios. Belgium and Italy sailed into the crisis with public debts of about 100% of GDP and yet did not end up with Troika programmes, while Ireland and Spain, with lowish debt ratios under 40%, needed bailouts. The real culprits were the large intra-eurozone capital flows that emerged in the decade before the crisis. These imbalances caused the build up of deep structural faults and fractures in the eurozone that would exploded in the 2010s. All the nations stricken by the crisis were running current account deficits. None of those running current account surpluses were hit.

When the eurozone crisis started, there was a ‘sudden stop’ in cross-border lending. Investors shaken by the global cessation in lending and generalised credit crisis, became reluctant to lend, especially to banks and governments in other nations. The special features of a monetary union meant that the ‘sudden stop’ of some credit mechanism in 2008 (which caused immediate problems in the US, UK and Icelandic financial systems) did not trigger an immediate crisis in the eurozone. Rather the global ‘sudden stop’ caused risk premiums on public and private debt to start to raise, the cost of borrowing began to escalate and the amount of credit started to dry up. The abrupt end of the capital flows that had sustained the speculative bubbles in the deficit eurozone countries raised concerns about the viability of banks and governments in nations dependent on foreign lending, i.e. those running current account deficits. Slowing growth produced big deficits and rapidly increasing public debt ratios. As the speculative asset and property bubbles burst banks were faced with catastrophic losses and the decision was taken that in order to save the banks several governments had to take on large amounts of their banks’ debt, thus increasing national debt ratios even further. This is how a balance of payments crisis became a public debt crisis.

The creation and design of the eurozone amplified the financial crisis in Europe

Burgeoning debt was not a Eurozone specific issue in the 2000s. Debt was also rapidly building up globally especially in the US, Britain and Japan. The period 2003-2007 was characterised by a very large increase in global credit with the global financial system bankrolling large net debt flows to advanced economies. The over supply of credit encouraged low interest rates which encouraged more credit creation and debt creation. At the same time an unprecedented wave of financial innovations (such as CDOs – collateralised debt obligations and CDS – credit default swaps) disguised the dangerously unsound and risky nature of much of the investment that was being funded and convinced the managers of the financial system that risk, by being shared, was being reduced. In fact all that was happening was that bankers and investment managers were losing track of what is it was they were actually investing in, losing track of the risks they were taking and toxic bad debt was being spread around the entire financial system.

In this dangerous mix, European monetary union mattered since it allowed the cross-border imbalances to get so large with such little notice. Eurozone membership also mattered since the incomplete institutional infrastructure amplifed the initial loss of trust in the deficit nations in several ways.

When both the banking system and government finances got into trouble in various eurozone member states there was no lender of last resort because the European Central Bank (ECB) had never been designed or mandated to act as a lender of last resort.

Having surrendered their national currency national central banks (which were now merely branch offices of the ECB) could not create money to lend to their government and the ECB was explicitly forbidden from doing so. Moreover the ECB at the time of the crisis did not act as lender of last resort for the various national banking systems that were in danger of collapsing. It was as if a hundred years of experience in how to head off or subdue a financial crisis had been dispensed with because without a lender of last resort a small debt failure or credit shock could be amplified without limit because every bank failure could cause yet further failures in a chain reaction. At the same time government bonds (a bed rock asset in the financial system) were losing value because the markets realised that there was no mechanism in place in the eurozone to rescue national governments, the result was that the cost of public borrowing for the peripheral countries began to rise sharply just as their borrowing needs were all rising sharply. The difference between developments in the UK, which had in the Bank of England as an active lender of last resort, and in the Eurozone is telling. This debt-default-risk vortex caught Portugal and came close to catching Italy, Spain and Belgium. Even France and Austria skated close to a generalised debt failure at the height of the crisis.

The other classic crisis response – devaluation – was impossible for eurozone nations.

By entering a currency union eurozone governments had not only given up control of monetary policy but they could also not devalue their currency. They had no lender of last resort and the only remaining national macroeconomic tool – fiscal policy – was heavily constrained by the rigid and rule based system for enforcing budget controls on eurozone member

The close links between eurozone banks and national governments greatly amplified and spread the crisis.

This is the so-called ‘doom loop’ – the potential for a vicious feedback cycle between banks and their government. It was one of the key reasons that a single surprise in Greece could swell into a systemic crisis of historic proportions (see my description of the financial ‘doomsday machine’ here).

In many eurozone nations, banks were thinly capitalised and extremely large relative to their countries’ GDP. They were so large that they had to be saved, but their size also created a ‘double drowning’ scenario, when the banks went down they took down the public finances as well. Ireland’s over leveraged banking system went down as borrowing costs rose and housing prices crashed. The Irish government went down trying to save its banks. Spain and Belgium flirted with, but ultimately avoided, the same fate. Cyprus was not so lucky.

The ‘doom loop’ also operated in the opposite direction. Eurozone banks tended to lend heavily to their own governments, especially as the crisis expanded. But absent an eurozone-wide bank resolution regime, this meant that the governments relied on the banks for the funds that would be needed for any eventual bank bailout. In this unstable situation, fears about the solvency of the banks fanned fears about governments’ solvency and vice versa, and this drove up government boring costs and this made things worse

The predominant role of bank financing in relation to investment and business credit in Europe transmitted bank problems to the wider economy far stronger than in the US.

As the ‘doom loop’ and slowing economy raised uncertainty, investment suffered much more than in countries where bank financing is less central, such as the US. This weakened economies in ways that worsened the sustainability outlook for nations and banks.

The rigidity of labour and product markets made the process of restoring competitiveness slow and painful in terms of lost output.

For all the talk of a common market for goods, labour and capital the European currency zone remains significantly more rigid than, say, the USA currency zone. Greek or Portuguese workers face far greater hurdles relocating to another member state (language, different national cultures etc) than US workers face relocating to another US state. Selling goods across EU borders is still more complex and challenging than selling goods across US state borders. This means that eurozone national economies, bereft of the sort of fiscal and monetary stimulus that could occur if they were not part of a currency union, and with their banking systems weakened by a lack of an effective lender of last resort, have found it very difficult to recover from the crash.

Just like in the Great Depression the problem is defined as being located in the deficit countries and never in the surplus countries.

It is the surplus countries, and above all Germany, that is in the driving seat in the eurozone. It was the decision by Germany to drastically hold down wages and its own domestic demand in order to build a large export based economy (aped by some other economies notably the Netherlands) that was the primary lever in the creation of destabilising imbalances in the eurozone. The problem is that the design of the eurozone regulatory system does not recognise surpluses as being a significant problem, the entire focus of the system is on reigning in deficits. In addition to the new central bank the currency union required building a new overarching European framework of macro-economic management and surveillance of member states public finances via the Stability and Growth Pact (SGP). As part of the Stability and Growth Pact the Macroeconomic Imbalance Procedure (MIP) surveillance mechanism was created that uses a scoreboard of indicators to identify countries whose economies are deemed as being problematic which can eventually lead to sanctions for euro area Member States if they repeatedly fail to meet their obligations. It is via the MIP, and its enforcement apparatus known as Excessive Imbalance Procedure (EIP) that the limits on government budget deficits and debt are set, but MIP also includes clauses about current account imbalances, capital flow imbalances etc. Whats very clear in these detailed rules and regulations is that some things are considered worse than others, and some things are not seen as a problem at all.

Using the EIP, the Commission can force countries into austerity when budget deficits and sovereign debts are too high, but can’t force them into stimulus or tax cuts when budget surpluses are high. It can force countries into wage moderation and real wage declines when wages rise too rapidly, but is powerless when wages rise too slowly. EIP will kick in when a country has a negative international investment position greater than -35%, but a high positive position goes unnoticed. It kicks in when inflation is too high, it does nothing when inflation is too low. Every indicator in the EIP is biased this way.

The result is that in a post crisis environment where it is persistent depression, unemployment and deflation that is the problem the entire weight and design of the eurozone architecture pushes economic policy in the wrong direction. Excessive government spending and inflation are not a problem in the eurozone, depression and deflation are the real problem but there are literally now no legitimate policy instruments left in the eurozone (other than the relatively ineffectual Quantitive Easing programs of the ECB) which can be used to reflate the economy.

The design of the eurozone has slowed recovery and prolonged economic depression

In a recent presentation to the FAROS Institutional Investors Forum Peter Praet, Member of the Executive Board of the ECB had this to say.

“The euro area economy is gradually emerging from a deep and protracted downturn. However, despite improvements over the last year, real GDP is still below the level of the first quarter of 2008. The picture is more striking still if one looks at where nominal growth would be now if pre-crisis trends had been maintained.”

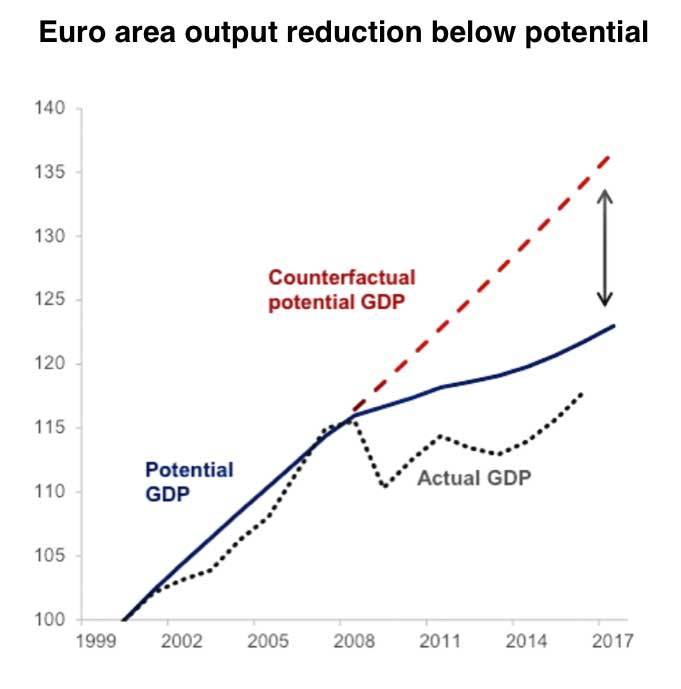

In his presentation Peter Praet presented a chart (below) which clearly shows the long term impact of the financial crisis. The chart shows what the potential GDP growth would have been if pre-crisis rates had been sustained, the current (estimated) potential output if the eurozone economy was working at full capacity, and the actual GDP of the eurozone since the the crisis. Its is the dotted line showing actual GDP that is so awful. Eurozone GDP is only now just creeping above its pre-crisis peak five years after the recession too hold.

The failure of the eurozone economy to recover after the recession and contraction is shown by the increase in the unemployment rate within the zone. The chart below is taken from the Eurostat August 2015 report and it shows unemployment across the EU rose after the crisis and how it rose further in the eurozone and has recovered less than in the non-euro parts of the EU.

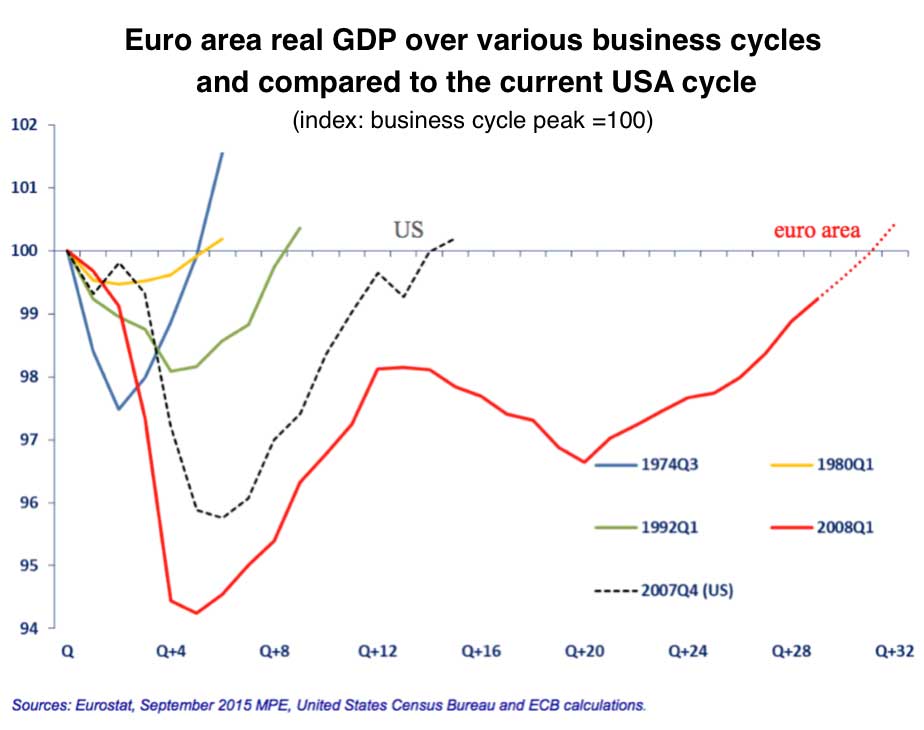

The fall in GDP growth between 2007 and 2015 has resulted in a rise in unemployment of nearly 4 percentage points. Currently, across the Euro area as a whole (population about 340m), adult unemployment stands at 11% and youth unemployment about twice that. Since 2008, the Euro area has experienced a severe, extended double-dip recession from which it has not yet emerged. Comparisons with previous recessions (see chart below) in Euro area countries (prior to the formation of the Euro, of course), as well as to the US’s 2009 recession, show just how severe and prolonged this recession has been. It is probably reasonable to call it a depression. The EU is the largest economy in the world and the eurozone makes up the largest segment of that economy. The design weaknesses of the eurozone have not only caused a prolonged depression in the EU but have contributed to the weakness of global recovery.

If the Euro area continues on the path shown in this chart, it should emerge from depression by the end of 2016. But as Praet observed in his presentation, the outlook for the global economy is not exactly bright, and the projected recovery path for the Euro area is by no means certain.

“The risks around the evolution of the global economy have shifted downward, making the contribution of external demand to the recovery less assured. Domestic demand, though rising, also appears relatively weak if one considers that we are still in an early phase of the recovery and that there are important tailwinds supporting the economy – namely our monetary stimulus and lower oil prices.”

As I have pointed out before the enforced shift to a low domestic demand export dependent economy in the eurozone, modelled on the German economy, makes the zone very vulnerable to shifts in the global economy.

There are other signs of serious weaknesses in the eurozone. Lending figures from the ECB for September 2015 show continuing weakness in private sector loan demand, largely offset by strong growth of general government borrowing (7.2%, up from 6.3% in August). Despite continuing attempts by Brussels/Berlin to squash government support in the name of “fiscal discipline”, it seems that governments are still borrowing to spend, which is good news because unfortunately there is little support coming from anywhere else.

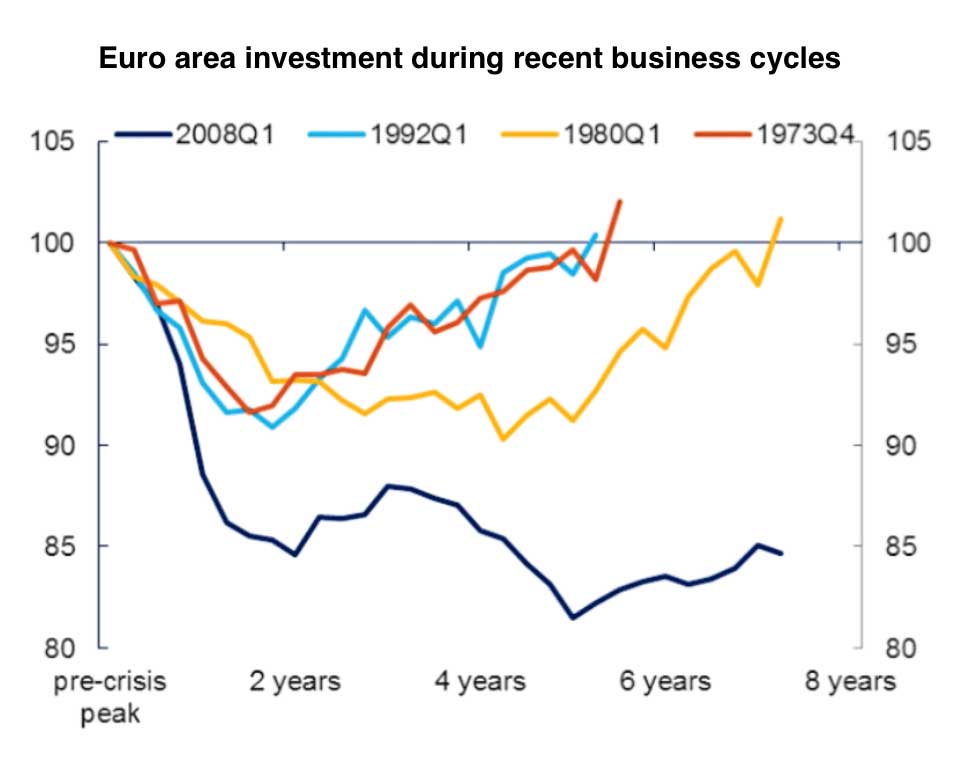

Investment in the Euro area fell sharply in 2008 and again in 2012, and remains shockingly low.

Praet observes that:

“investment has so far failed to perform its “accelerator” role for the recovery.”

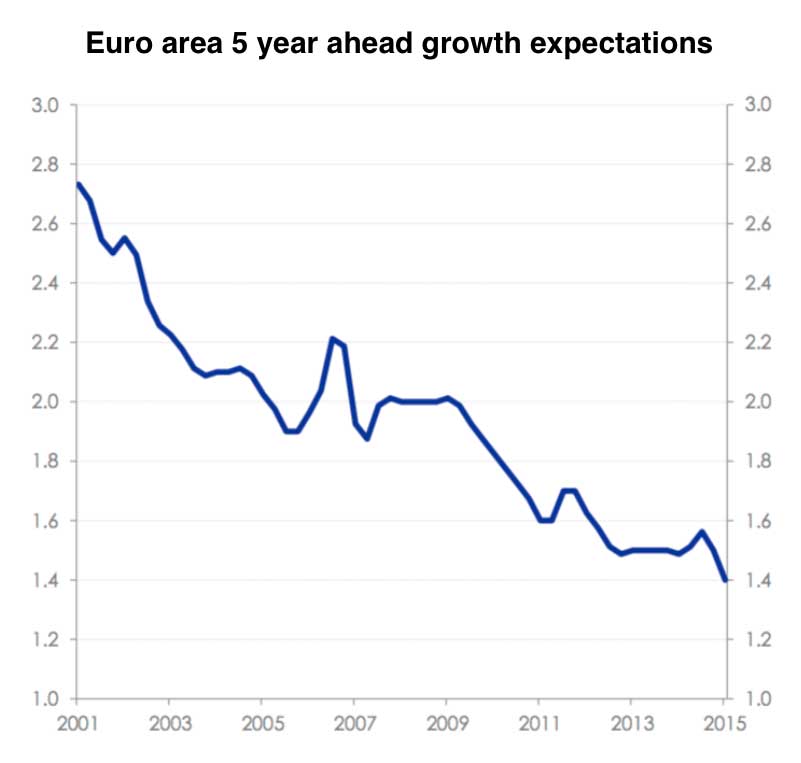

He goes on to attribute this to the continuing overhang of private and public sector debt, and to the very poor returns on capital in some Euro area countries. Importantly, Praet also notes that expectations of future growth in the Euro area are declining. The debt overhang is undoubtedly part of the cause of the investment chill, but so are the low expectations of investors. If eurozone businesses expect GDP growth over the next five years hence to be a pathetic 1.4%, and if domestic demand continues to remain deliberately depressed (in the name of fiscal discipline) why would they bother to invest?

The outlook for the eurozone is not good

The Euro area is stuck in a low-growth, low-inflation, high-unemployment equilibrium. As Keynes demonstrated in his book ‘The General Theory of Employment, Interest and Money’, which was published nearly eighty years ago, that an economy can settle at equilibrium points below full capacity and that depressed economic conditions and high unemployment can become entrenched. In order to knock an economy out of this low equilibrium point and back up to an equilibrium of greater activity and lower unemployment both strongly expansionary monetary and fiscal policies are required. The countries in the Euro area don’t have freedom anymore to pursue such policies. Monetary policy is now beyond their control (it is controlled by the ECB which was designed to be immune to any democratic control with a remit to ensure price stablity) and they are restricted by fiscal rules that make it impossible for them to do the large-scale investment spending that will be needed to restore growth. There is no Euro area federal government that could take on an investment programme of the necessary scale, the insipid proposals being touted as the Juncker’s plan are ridiculously inadequate. The ECB is the only player with the necessary firepower, but it is insanely prevented by treaty directive from using its really big monetary guns.

The general consensus narrative in the EU argues that restoring growth requires yet more “structural reforms” from governments (code for unemployment leading to lower wages and a more’flexible’ workforce), not for a more active role for the ECB, or indeed any pan-European initiative of any real substance. It was the ECB itself that triggered the double-dip recession by failing to do its job of lender of last resort, allowing the Euro to fragment and sovereign yields to spike due to fears of Euro breakup and possible redenomination of debts, and by absurdly pushing up intererest rates and tightening monetary policy even before the initial wave of recessionary contraction had finished.

Although the high crisis of the euro has subsided its inherent weakness as a monetary system remains. There are no mechanism for dealing with the uneven economic performance of the various national regions of the eurozone other than mass unemployment and impoverishment. I can see no way that the eurozone economy, currently in a depressed state, will return to a rate of growth high enough to seriously dent the unemployment rate in the foreseeable future, and the zone as a whole is now moving towards being heavily dependent on exports markets just as global growth slows down. I think any reasonable person would agree that the single currency project has been a failure in that it has delivered neither economic stability, prosperity nor political solidarity.

It is what to do about that failure that is the difficult question.